Legal Business 100: Main Menu Legal Business Overview Marathon, not a sprint Events since coronavirus hit should have triggered a crisis of epic proportions. But our LB100…

LB100: Methodology and notes Legal Business LB100 LAW FIRMS The firms that appear in the Legal Business 100 (LB100) are the top 100 law firms in…

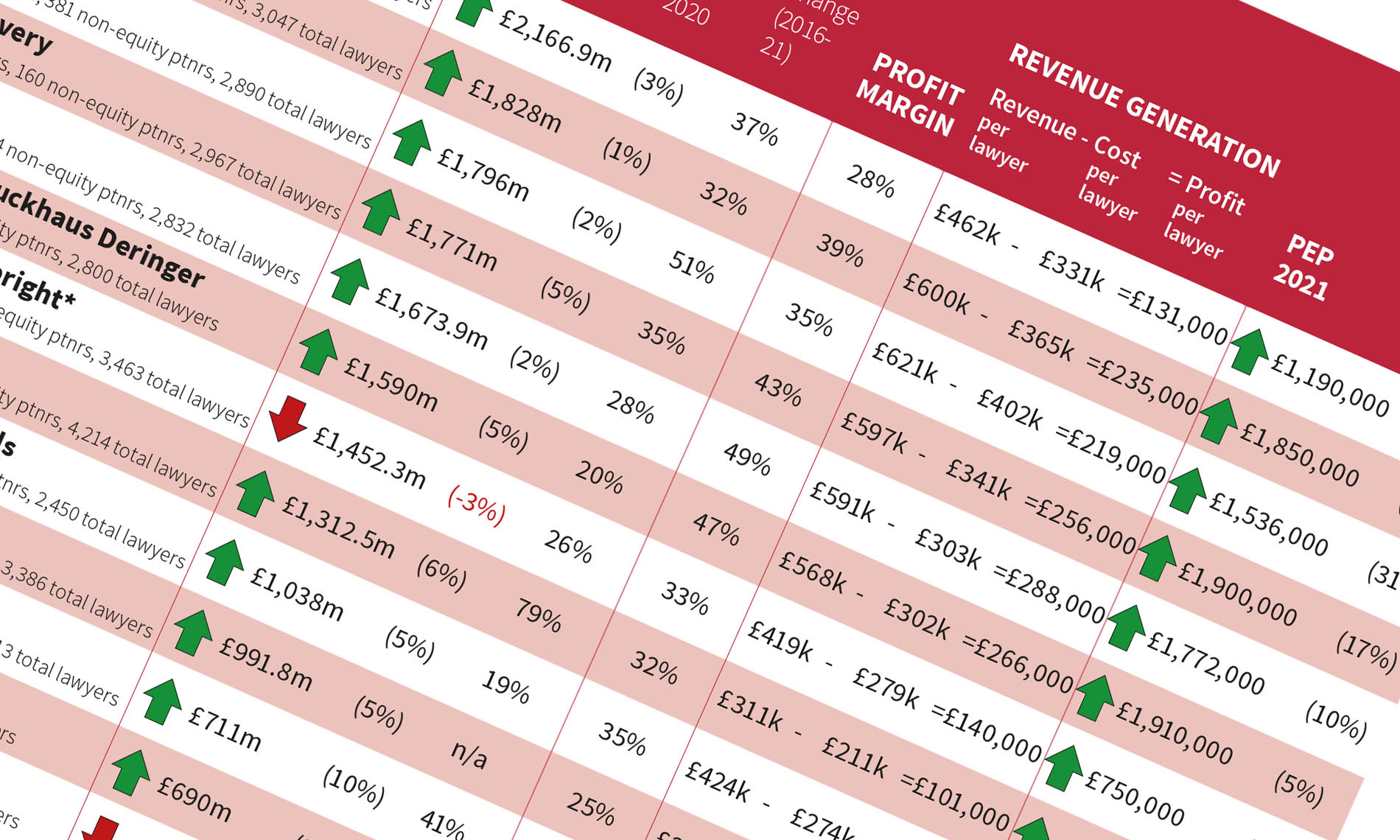

LB100 Overview: Marathon, not a sprint Nathalie Tidman The phrase has long been a cliché among industry circles, but no-one is better at being cautiously optimistic than a…

LB100 Second 25: The great leap upwards Tom Baker Analysing and then explaining the performance of the LB100’s 26-50 bracket is far from straightforward. The monumental disruption of the last…

LB100 Second 50: Regional View – Faster, higher, stronger Mark McAteer The regional and smaller national firms that sit in the 51-100 bracket of the Legal Business 100 (LB100) have again…

LB100 Second 50: City and Boutique – Percentage play Mark McAteer The 21 London-based firms that sit in the second half of the LB100, many of which are specialist, focused players,…