LB100: Shipping and Insurance – Peaks and Troughs

If the post-Lehman years have in general been good to the City’s insurance and shipping specialists, 2013/14 has been a…

If the post-Lehman years have in general been good to the City’s insurance and shipping specialists, 2013/14 has been a…

The LB100’s regional players have seen starkly divided fortunes with the South West players sailing ahead while northern firms face choppy…

While the headline Legal Business 100 (LB100) results are once again inflated by significant merger activity at every level, there…

Consolidating firms are jostling for position in the race to dominate international and UK markets. But even amid fairer conditions,…

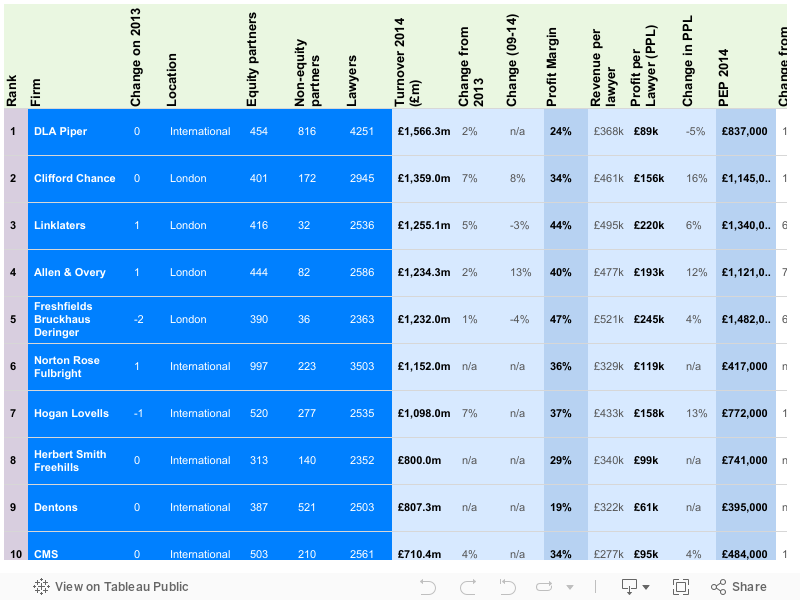

LB100 LAW FIRMS The firms that appear in the LB100 are the top 100 firms in the UK, ranked by…

Core Stats from the LB100 2014. Includes; Ten fastest growing firms by revenue, Ten fastest shrinking firms by revenue, LB100…

Which firms are the most profitable? In this table we blend together all of our profitability measures, including PEP, profit…

From collaboration to rough quarters to restoring market confidence, leaders at Legal Business 100 firms give us their views on…

A better year but not every LB100 firm can navigate the choppy waters.

Menu The Top 25 – Wind in their Sails LB100 2014: The Main Table The Second Quartile – Close Hauled…

While the headline Legal Business 100 (LB100) results are once again inflated by significant merger activity at every level, there…